Good Governance. Greater Returns.

Why corporate governance is the key to an ESG-friendly portfolio

Environmental, Social and Governance (ESG) issues are taking a larger place in investor mindsets of late. As the Green Revolution takes hold, corporations’ roles in protecting our planet has driven their environmental practices to the forefront.

At the same time, global companies’ treatment of workers in factories and warehouses has ignited debates about corporate social responsibility. Given these, one can be forgiven for believing that the third letter in the ESG framework – governance – should take a backseat to environmental and social issues.

We would fervently disagree. In our experience, corporate governance – the system of rules, practices and processes by which a corporation is controlled and operated – is the most critical and impactful of the three ESG factors, as it is arguably the only one that can influence the other two. To us, corporate governance is the soul of a corporation – starting from the top, it dictates and permeates down into the firm’s culture, and ultimately determines its integrity, ethics and fairness in all matters, including environmental and social ones. In short, success in firm governance tends to lead to successes in environmental and social issues as well.

The window to the corporate soul

If you really want to see inside a company and figure out what makes it tick, open up a proxy circular. Detailing what issues will be presented and voted on at the next shareholder meeting, it provides a treasure trove of useful insights on the company’s management team and its board of directors: What’s the average director tenure? How independent are the directors? Are managers incentivized to deliver long-term success, or is short-termism an issue? If governance is the soul of a corporation, then proxies are the window to that soul. That’s why our team reviews and votes every proxy ourselves – they provide such valuable insight into the firm’s potential to generate long-term value that neglecting to vote them would be damaging to our portfolio’s performance at best, and downright irresponsible at worst.

But proxies aren’t our only way of monitoring and influencing corporate governance. We are in the enviable position of being not only large shareholders of many companies, but perhaps more importantly, of being long-term holders. With a turnover rate around 10%, our average holding period is about 10 years. This long holding period results in very healthy relationships with corporate management teams, who come to know us as partners who aren’t looking to start battles, but rather to engage with them and help them improve their practices, creating shareholder value over the long term.

For example, through a regular governance check on one of our long-held names, we came to be uncomfortable with the lack of independence of several board members. After raising our concerns with the company, we agreed that upon the nearing retirement of these two board members, their successors would be independent – a change which occurred shortly thereafter. We also expressed our concerns about their CEO sitting on the nomination committee – in the months that followed, they removed him from that committee. Did these engagements cause any animosity between our team and their board? Quite the opposite. Recognizing that our goal is to do what’s best for shareholders in the long-run, some time later, the same company in fact approached us for our advice and opinions on upcoming changes to their compensation structure, demonstrating the way in which we affect corporate governance is a two-way street.

The portfolio management industry often prides itself on its engagement with and influence on corporations. While this is certainly true in many cases, the fact is that the average share holding period for our peers investing in the global large cap universe is just over two years. Even worse, globally, the average holding period for a share traded by any stock market participant is a mere 11.5 months!1 Surely that’s not enough time to develop a constructive relationship with a corporation – we’ve spent more time analyzing some companies than our peers do holding them – and thus we are doubtful that managers are constructively engaging with their portfolio companies as much as they claim. Still, we were surprised when we approached one of our portfolio companies – which has been public for nearly four decades and has over 500 institutional holders – to request some clarification and context regarding their compensation scheme; management told us that they’d have to look into how they could handle our inquiry, as it was the first of its type they’d ever received. So, while our industry certainly has the clout and ability to positively influence corporate governance decisions, there is clearly wide dispersion between the managers that actually do it and those that don’t.

Source: Fiera Capital, data via eVestment. Averages using yearly data from 2009 to 2019.

Regarding the former, our proprietary ranking process explicitly seeks to identify potential ESG issues in the form of risks and red flags. When scoring an investment opportunity, if a potential risk related to any of the three ESG elements exists, it reduces the investment’s attractiveness and therefore its likelihood of making it into the portfolio. To us, an ESG risk will inevitably translate into a financial risk to our portfolio and thus it carries as much weight in our process as any other type of risk. That’s why flagging potential Environmental, Social and Governance issues early on in the scoring process is so critical – without it, we would be overlooking potential detractors from performance.

Source: Fiera Capital.

On a more implicit level, we incorporate ESG factors through our basic investment philosophy: high quality. The metrics on which we focus – namely, low capital requirements, high margins, and high and sustainable return on capital – demand that our portfolio companies be efficient in everything they do. After all, efficiency in the use of resources – for example, due to waste reduction or lower energy use – will be reflected in corporate financials in the form of higher margins and lower capital requirements. Consequently, highly efficient firms are more attractive to us from a quality perspective and therefore from an investment standpoint as well.

Efficiency in the production of goods is critical, but the quality effect is even more pronounced if the company‘s output – that is, its products – is efficient for the end user. For example, one of our holdings is a world-leading manufacturer of fluids and coatings equipment. They produce (among other things) paint guns for the automobile industry which are far more efficient than their peers’, meaning they use less paint. Less paint means lower input costs for the end user, incentivizing them to use this particular paint gun. The end result is that this portfolio company has significant pricing power, which we believe is a major contributor to long-term profitability.

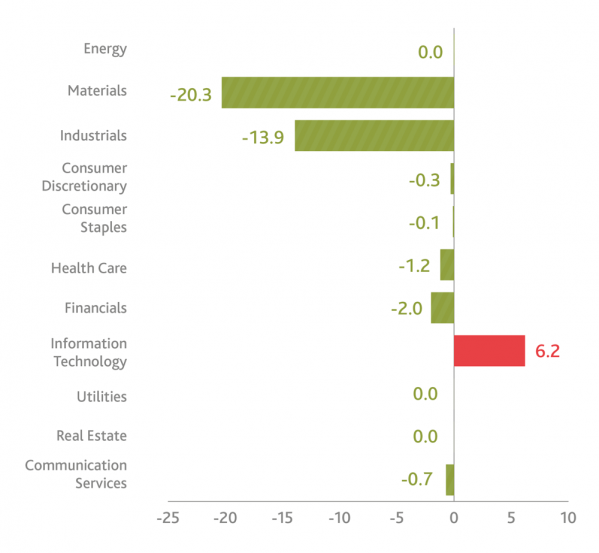

One can see the results of how our quality bias affects the environmental aspect of our portfolio by examining its carbon footprint. As of the first quarter of 2020, our flagship strategy’s carbon intensity (in terms of tons of CO2 equivalent emissions per millions of dollars of revenue) was 33.2, one-fifth of its benchmark (the MSCI World Index). Undoubtedly, some of this reflects the fact that we hold no energy or utilities names, which are two highly-polluting sectors. Yet if we look deeper, we can see that security selection within each sector reduces our carbon intensity impact versus the benchmark for all but one of the sectors in which we invest.

Global Equity strategy – weighted average carbon intensity, attribution vs benchmark (MSCI World Index)

Source: GHG Emissions data based on GHG Scope 1 and 2 Emissions as of 03/31/2020; data via MSCI ESG Manager. Portfolio and index holdings as of 03/31/2020. Data via Fiera Capital, Eagle Data Management.

Is this significantly lower carbon intensity a result of us seeking out low-carbon companies? Admittedly, no. It’s a fortunate consequence – though not a coincidence – of the fact that we seek the most efficient and sustainable companies over the long term. It just so happens that an efficient company is often a successful one.

Global Equity strategy – weighted average carbon intensity, security selection effect vs benchmark (MSCI World Index), by GICS sector

Source: GHG Emissions data based on GHG Scope 1 and 2 Emissions as of 03/31/2020; data via MSCI ESG Manager. Portfolio and index holdings as of 03/31/2020. Data via Fiera Capital, Eagle Data Management.

Honesty is the best ESG policy

In our view, a long-term investment horizon and an emphasis on strong corporate governance go hand in hand – finding companies who are strong on the latter makes us comfortable owning them for long periods of time. This enables constructive relationships with management teams, which in turn helps drive positive social and environmental aspects as well as deliver financial value for shareholders. Put differently, our focus on the governance aspect within ESG is not an accident: it gives us a window into the soul of the corporation, and we believe it leads to a more sincere and honest approach of integrating ESG aspects into our portfolios. After all, if you can understand a company’s governance and the corporate culture which it drives, you’ll get a truly undistorted picture of its actual environmental and social impacts. Perhaps more importantly, if you can influence that soul through proxy votes and dialogue with its leaders, you can drive its ESG policies into better directions.

Our investment philosophy has always been to build a high-quality portfolio from a risk and return perspective. By engaging with current and potential companies, we’ve found that success in corporate governance begets success in environmental, social and even financial aspects as well.

Is our emphasis on governance unique? Unlikely. But it does result in ESG attributes that are transparent, honest, and contributors to long-term returns.

1 World Federation of Exchanges database, via the World Bank Data Catalog. data.worldbank.org/indicator/CM.MKT.TRNR. Data as of 2018.

Related Insights

Q2 2026 Sustainability Update