Is the Bond Market Getting Ahead of Itself?

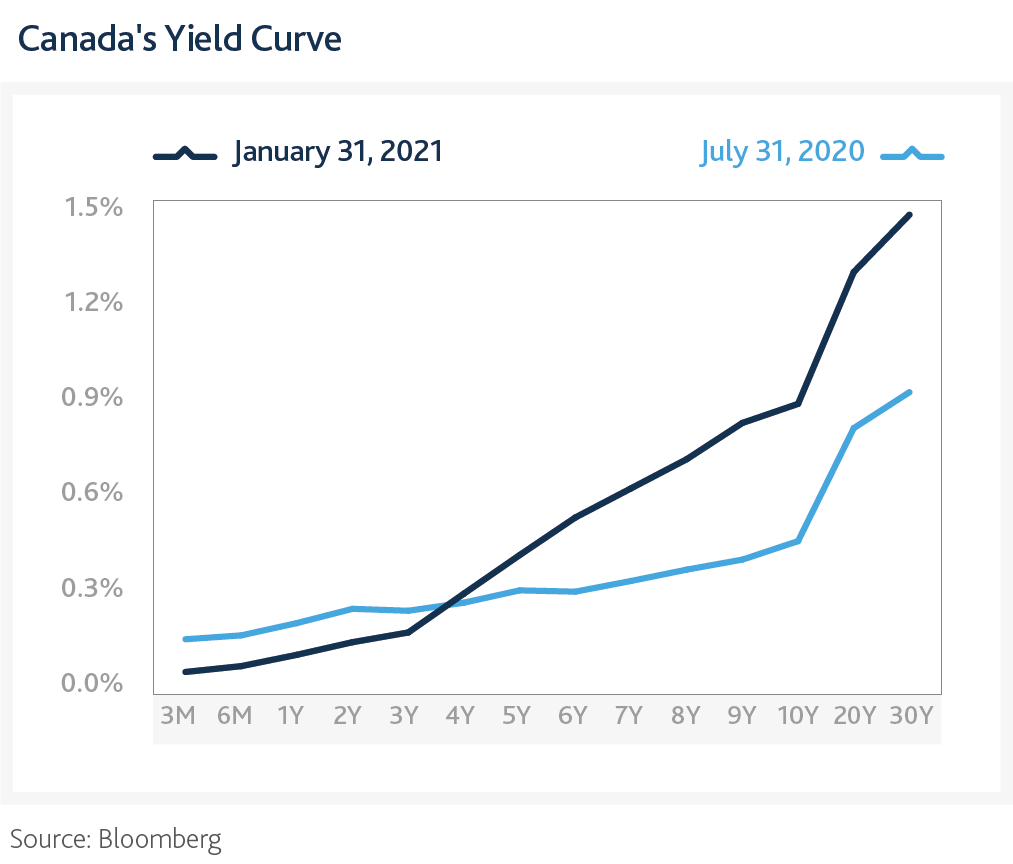

As we can see in the chart below, the shape of the yield curve has changed significantly over the past six months, steepening thanks to both the short and long ends of the curve. Short-term rates have decreased, as the Bank of Canada announced that it will most likely keep its current accommodative monetary policy until 2023. Traders even started pricing in a small rate cut. Meanwhile, long-term yields have moved higher on hopes of a swift economic recovery and successful vaccination programs, as well as increased inflation expectations.

True, financial markets are forward-looking, but we believe that the answer to the above question is yes. In our opinion, the bond market is currently overlooking the lasting impact that risks such as a slow vaccine rollout and the spread of new COVID variants could have on the overall economy. Moreover, the economic recovery is mostly contingent upon the governments’ ability to pass timely stimulus bills, which have the history of experiencing delays. For instance, Canadian airlines are still waiting on a muchneeded aid package from Ottawa. Treasury Secretary Janet Yellen even warned that “if we don’t provide additional support, the unemployment rate (in the U.S.) is going to stay elevated for years to come.” Regarding inflation, we believe that while the Federal Reserve’s framework now allows inflation to overshoot its target of 2%, deflationary factors such as the globalization, lower tariff risks under President Joe Biden, and increased productivity are also at play, limiting the potential upside for prices.

Thus, as a lot of good news is now priced-in by the market, we decided to lengthen our duration; buying long-term bonds to protect against potential short-term shocks.

Related Insights

Global Asset Allocation Team Market Update – July 2026

Canadian Yield Curve Overview

Q3 2026 Investment Outlook & Portfolio Strategy