Don’t Fight the Fed

At some point in their career, all active portfolio managers will inevitably ask themselves if they are being too active. After all, they are paid to generate additional returns beyond those of the market, and thus they may fear that being positioned too close to the index is doing their client a disservice. But humble fund managers must also accept the need to choose one’s battles, and to know when they’re outmatched.

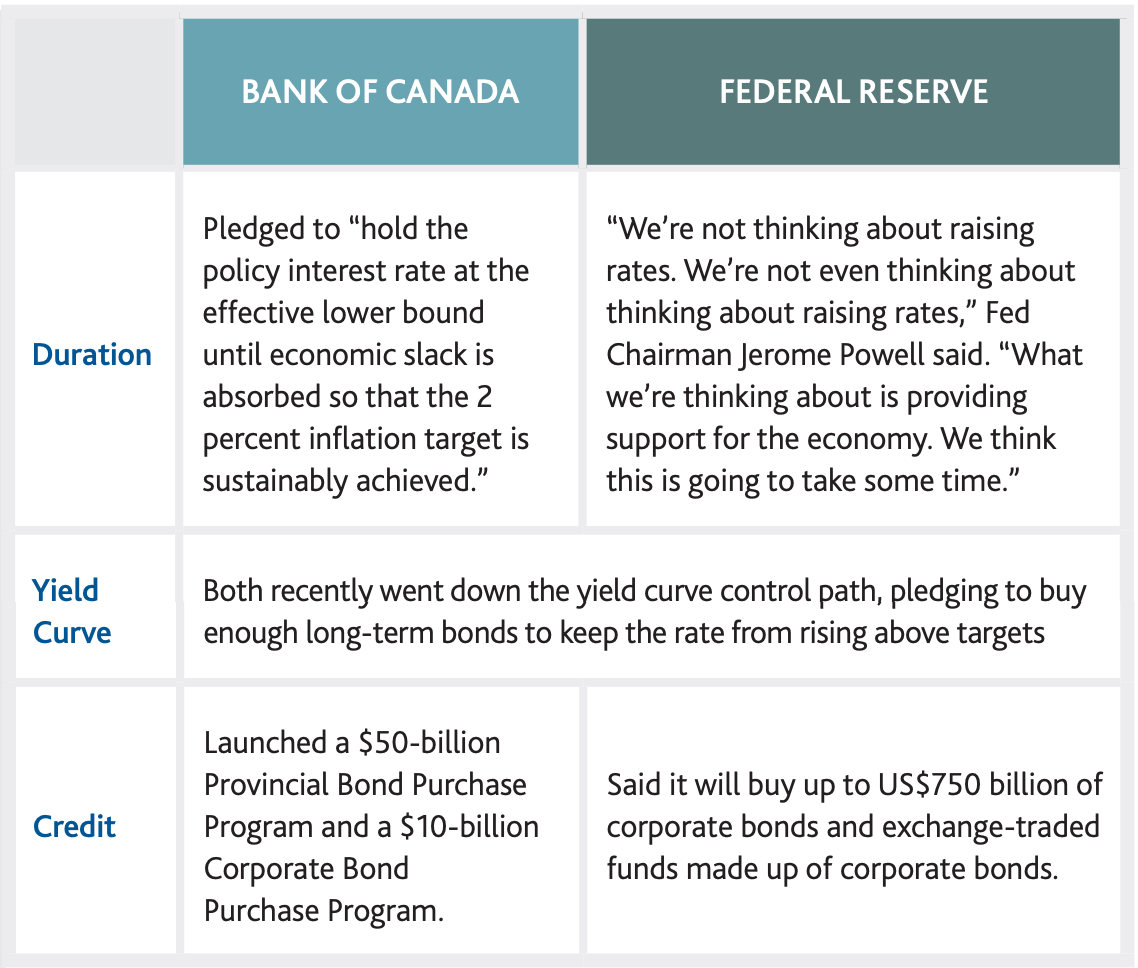

There are three major sources of value add for active bond managers: duration; curve positioning; and credit exposure. Historically, our team has taken a contrarian approach to the markets, so we’re used to be having significant deviations from our benchmark on those fronts. However, the Bank of Canada and the Federal Reserve have made their intentions crystal clear in the near term – they have anchored short-term yields lower to bolster the economy; they are buying long-term issues in order to keep a flatter yield curve (to help finance their governments’ huge stimulus measures); and they are buying corporate – and, in the case of the BoC, provincial – bonds to provide liquidity to the bond market and support credit products. Given this, we’re of the belief that going up against these two financial behemoths is not a battle worth fighting.

Thus, as it stands, we find ourselves uncharacteristically deviating only slightly from the market, as the central bank’s actions are mainly dictating ours. As highly active managers, this should feel uncomfortable. But it doesn’t, as we truly feel that being positioned this way offers the best risk/reward for our clients. Why? At the moment, we are preparing for both a risk-on and risk-off environment; there are simply too many unknowns and “ifs” driving the market: will there be a second wave of COVID-19?; if there is, will the economy go back into lockdown?; if it does, do corporate bonds fall (due to a flight to safety) or rally (on hopes of increased fiscal stimulus and central bank programs)?

In truth, no fund manager can predict the future or answer these questions with certainty, but one thing is for sure: the central banks’ programs will continue to be one of, if not the, primary drivers of bond markets. Our job is to properly price the risks facing our clients and decide if a bet is worth taking. If this means having to deviate somewhat from our traditional management style and be more in-line with the universe on some aspects than we would normally be, so be it. Better that than to go toe-to-toe with two of the most powerful financial agents in the world.

Disclosures

This information is prepared by Fiera Capital Corporation (“Fiera Capital”) and is intended for use by residents of Canada only. The information and opinions expressed herein are provided for informational purposes only, are subject to change and should not be relied upon as the basis of any investment or disposition decisions. Past performance is no guarantee of future results. All investments pose the risk of loss and there is no guarantee that any of the benefits expressed herein will be achieved or realized. Valuations and returns are computed and stated in Canadian dollars, unless otherwise noted.

The information provided herein does not constitute investment advice and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell a security. It does not take into account any investor’s particular investment objectives, strategies, tax status or investment horizon. There is no representation or warranty as to the current accuracy of, nor liability for, decisions based on such information. Any opinions expressed herein reflect a judgment at the date of publication and are subject to change. Although statements of fact and data contained in this presentation have been obtained from, and are based upon, sources that we believe to be reliable, we do not guarantee their accuracy, and any such information may be incomplete or condensed. No liability will be accepted for any direct, indirect or consequential loss or damage of any kind arising out of the use of all or any of this material.

Views expressed regarding a particular company, security, industry or market sector should not be considered an indication of trading intent of any funds or accounts managed by any Fiera Capital entity. Each entity of Fiera Capital only provides investment advisory services or offers investment funds in the jurisdictions where such member and/or the relevant product is registered or authorized to provide such services pursuant to an exemption from such registration.

Related Insights

Global Asset Allocation Team Market Update – May 2026

Canadian Yield Curve Overview

Global Asset Allocation Team Market Update – June 2026